Your CPM jumped 34% this quarter, your CTV vendor can’t explain attribution past a 7-day window, and three agencies just pitched you “AI-powered programmatic” with nearly identical decks. Sound familiar? Media buying in the United States has gotten harder, not easier, even with smarter tools and bigger budgets on the table.

This guide cuts through the noise. You’ll see what the US ad market actually looks like in 2026, how spend is shifting between CTV, retail media, and walled gardens, and which buying models pay off for B2B brands versus DTC. You’ll get a framework for vetting agencies, benchmark CPMs by channel, and the contract terms most marketers miss until renewal.

Whether you run a $2M annual budget or $200M, media buying in the United States rewards operators who ask sharper questions. Let’s get into them.

Key Takeaways

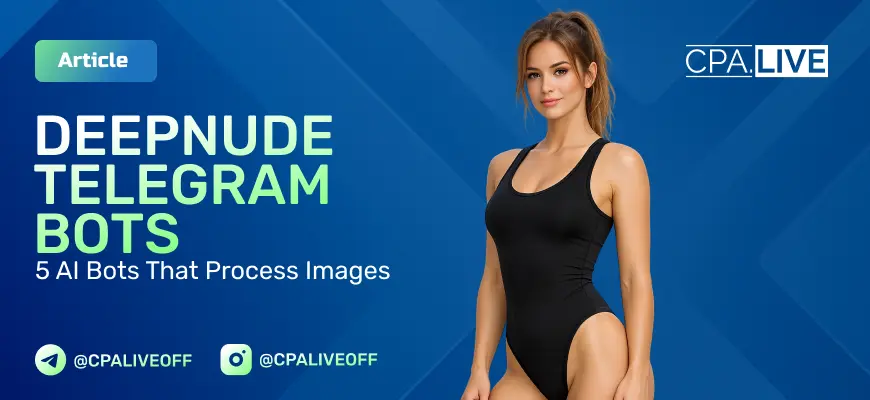

- Omnicom completed its merger with Interpublic Group on November 26, 2025, creating a $26 billion holding company with 1,500 agencies and targeting $1.5 billion in cost savings.

- US CTV upfront ad spending will hit $17.73 billion in 2026, surpassing primetime linear TV’s $16.98 billion for the first time, with 84% of CTV spend now transacted programmatically.

- Private marketplaces accounted for over 92% of median programmatic spend and 100% of CTV transactions in Q4 2025, per the ANA’s Programmatic Transparency Benchmark.

- Principal-based media buying is expanding — 56% of marketers expect to use it in the coming year, but only 57% have guidelines in place, and 90% worry it conflicts with their interests.

- Brands under $3M in annual media spend usually win with an agency, while $10M+ advertisers typically bring paid search and social in-house and keep agencies for CTV, linear, and complex programmatic.

What media buying actually means in the US market

Media buying in the United States is the negotiation and purchase of ad inventory across TV, radio, print, out-of-home, digital, CTV, and audio channels — the execution layer that turns a marketing strategy into placed ads at agreed rates. The US government classifies the discipline under NAICS code 541830 (Media Buying Agencies), which covers establishments primarily engaged in purchasing advertising time or space from media outlets and reselling it directly to advertising agencies or individual companies, per the Census Bureau / IBISWorld NAICS reference.

Buyers work with two basic things: inventory (the ad slots themselves, from a :30 spot on local broadcast to a programmatic CTV impression) and the deal structure around them — CPM, CPP, GRP guarantees, makegoods, upfront commitments, or open-auction RTB.

Two functions often get blurred, so let’s separate them:

| Media planning | Media buying | |

|---|---|---|

| Inputs | Brand goals, audience research, budget, brand safety rules | Approved plan, rate cards, inventory availability |

| Outputs | Channel mix, flighting, target reach/frequency | Insertion orders, IOs, programmatic deal IDs, placed buys |

| KPIs | Reach, frequency, share of voice, projected ROAS | CPM delivered vs. planned, fill rate, pacing, post-log accuracy |

| Owner | Strategist / planner | Buyer / activation team |

The US market is unusually hard to navigate for three reasons. Geography: Nielsen splits the country into 210 DMA® regions in total, covering the entire continental U.S., Hawaii, and parts of Alaska, with each county exclusively assigned to one market, per Nielsen’s DMA reference. Digital fragmentation: dozens of DSPs, SSPs, walled gardens, and retail media networks all hold meaningful inventory. And regulation: state-level privacy laws (CCPA/CPRA in California, plus newer regimes in Virginia, Colorado, Texas, and others) change what audience data you can actually buy against.

The 2026 US media buying landscape: size, players, and the Omnicom–IPG shake-up

US media buying in 2026 has been reshaped by the largest agency merger in history. The Omnicom–IPG deal closed in late 2025 — specifically, Omnicom Group Inc. completed its merger with The Interpublic Group of Companies on November 26, 2025, exchanging each IPG share for 0.344 Omnicom shares and creating a combined company roughly 60.6% owned by legacy Omnicom shareholders and 39.4% by legacy IPG shareholders, according to Omnicom’s SEC 10-K filing. Adweek reports the deal yielded a holding company with $26 billion in revenue and 1,500 agencies, pushing the combined entity to the top of the global holding company ranking ahead of WPP and Publicis.

Holding companies that dominate US buying. Six holding companies still control the bulk of US media investment: Omnicom (now including IPG), WPP GroupM, Publicis, Dentsu, Havas, and Stagwell. Combined, they place the majority of national TV, CTV, and programmatic spend through centralized investment desks like OMG, GroupM, and Publicis Media. Their leverage comes from volume commitments at the upfronts and direct API integrations with the major DSPs.

What the Omnicom–IPG merger changes for clients. Holding company consolidation at this scale means fewer independent negotiating tables. Clients of Mediabrands (IPG) and OMG now sit under one roof, which raises real conflict-of-interest questions for competing brands — think two QSR chains or two auto OEMs suddenly sharing a parent. Expect contract reopeners in 2026, more aggressive performance guarantees, and pressure on fees. According to Mission Media, Omnicom has doubled its total cost savings target from US$750 million to US$1.5 billion, with US$900 million expected in 2026 alone — pressure that will inevitably reach client fees and staffing models. On the upside, the merged group has deeper first-party data assets and stronger CTV inventory deals. Publicis has countered with its own data-and-AI investments, doubling down on identity and generative creative capabilities.

Where independents still win. Boutique shops like Horizon Media, Tinuiti, and Wpromote keep winning when clients want senior attention, channel specialization (retail media, performance, CTV), or freedom from holding company conflicts. For brands under $50M in annual ad spend, an independent often delivers better margins and faster decisions than a network desk.

Traditional vs digital media buying in the US

The line between traditional and digital buying has mostly collapsed. A 30-second spot now runs across linear broadcast TV, connected TV, and YouTube from the same plan, often through the same holding company. But how you actually purchase that inventory — and what you pay for it — still splits cleanly into two worlds.

How traditional channels are bought

Linear TV, radio, print, and OOH are bought on reach and frequency. Broadcast TV deals get locked in at the upfronts each May, where networks sell 60–80% of their fall inventory to advertisers at negotiated rates. Pricing is benchmarked against Nielsen ratings and quoted in GRPs (Gross Rating Points) — one GRP equals 1% of your target audience reached once. Scatter market buys fill in the rest closer to air date, usually at a 10–25% premium. OOH (billboards, transit, place-based screens) is bought by impression counts from Geopath, in 4-week flights, market by market.

How digital channels are bought

Digital runs on auctions and APIs. Display, paid social, paid search, CTV/OTT advertising, and streaming audio all clear through real-time bidding or biddable platforms (Google, Meta, Amazon, The Trade Desk). You buy audiences, not dayparts. CTV crossed a structural line this year: per eMarketer forecasts cited by Digital Applied, in 2026, US CTV upfront ad spending of $17.73 billion will exceed primetime linear TV upfront spending of $16.98 billion — the first time streaming has out-committed primetime linear.

| Channel | How it’s bought | Typical 2026 US CPM | Best for |

|---|---|---|---|

| Broadcast TV | Upfront + scatter, GRP-based | $25–$45 | Mass reach, B2C launches |

| Cable TV | Upfront + scatter | $15–$30 | Targeted demos |

| CTV/OTT | Programmatic + direct | $35–$60 | Cord-cutters, premium B2C |

| Paid social | Auction (CPM/CPC) | $8–$25 | B2C performance, B2B lead gen |

| Paid search | Auction (CPC) | $2–$8 CPC | Intent capture |

| OOH (digital) | Programmatic DOOH + direct | $5–$15 | Local awareness |

| Podcast/streaming audio | Host-read + programmatic | $18–$35 | B2B trust, niche B2C |

Channel mix logic. B2C brands chasing scale still anchor on CTV plus paid social, with broadcast TV reserved for tentpole moments. B2B advertisers skew toward LinkedIn, paid search, podcast sponsorships, and increasingly programmatic display against firmographic audiences — GRPs rarely enter the conversation.

On the buying side, I keep seeing teams overpay for CTV because they treat it like linear and skip the deal-ID hygiene. On the last few US runs we did, swapping out a couple of open-exchange CTV lines for curated PMPs with three premium publishers dropped effective CPM from around $52 to the high $30s without losing completion rate. The lazy fix is to chase cheap CPMs in open auction — and that’s exactly where the MFA traffic and weird co-viewing inflation lives.

How programmatic buying works in the US (RTB, DSPs, and deal types)

Programmatic now drives the vast majority of US digital display spend, meaning most ad buys happen through automated auctions rather than direct insertion orders. Within CTV alone, The Gutenberg notes that 84% of CTV ad spend is now transacted programmatically.

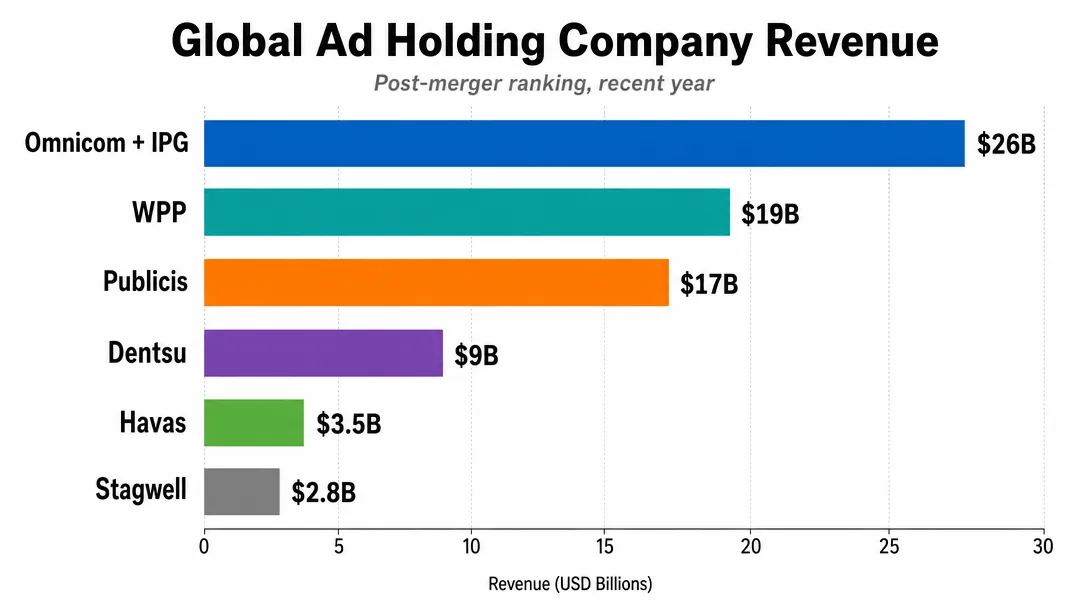

The RTB flow in under 300ms

When a user loads a page or streams a CTV show, the publisher’s supply-side platform (SSP) sends a bid request to multiple demand-side platforms (DSPs). Each DSP evaluates the impression against your campaign rules — audience match, frequency cap, budget pacing — and returns a bid. Highest eligible bid wins, the ad serves, and the user sees it. Total time: under 300 milliseconds. That’s real-time bidding (RTB).

Open exchange vs PMP vs programmatic guaranteed

Three deal types cover most US buys:

- Open exchange. Public auction, broadest inventory, lowest CPMs, weakest brand safety controls. Best for prospecting and scale.

- Private marketplace (PMP). Invite-only auction with pre-vetted publishers and negotiated floor prices. Better quality, more transparency, modest premium. PMPs now dominate the high-quality end of the market — the ANA’s Q4 2025 Programmatic Transparency Benchmark found private marketplaces accounted for over 92% of median spend across environments and 100% of CTV transactions.

- Programmatic guaranteed. Fixed price, fixed volume, locked inventory — automation without the auction. Best for tentpole campaigns, premium CTV slots, or homepage takeovers.

Major DSPs. The Trade Desk leads the independent side, especially for CTV and retail media. Google’s DV360 dominates buys tied to YouTube and Google inventory. Amazon DSP unlocks Amazon’s shopper data and Prime Video, and its DSP partnerships now reach into Netflix’s inventory as well, per Digiday. Yahoo DSP remains relevant for native and East Coast publisher relationships.

First-party data without third-party cookies. With third-party cookies effectively gone in Chrome, identity runs on first-party data: CRM lists, hashed emails, and onboarding into IDs like UID2 and RampID. Clean rooms (Amazon Marketing Cloud, LiveRamp, Google Ads Data Hub) let you activate that data inside a DSP without exposing the raw records. For independent buying teams running their own DSP seats, the operational side — funding accounts, issuing cards to media buyers, and managing payment limits across platforms — often runs through purpose-built financial platforms for media buying teams rather than traditional banks.

AI and agentic systems are rewriting US media buying

Most US ad buyers already use or plan to deploy AI-powered buying tools, reframing AI from experiment to default operating layer across the stack.

Platform-native AI dominates the walled gardens. Meta Advantage+ Shopping campaigns collapse audience, creative, and placement decisions into a single optimization loop. Google Performance Max runs across Search, YouTube, Display, Discover, and Gmail from one asset set and one goal. Amazon Ads layers similar automation on top of first-party retail signals. On the open web, The Trade Desk’s bidding AI surfaces audience expansion and bid recommendations inside the DSP, and Criteo’s commerce platform applies the same logic to retail and commerce inventory.

The next layer is agentic AI: autonomous agents that brief a campaign, generate creative variants, launch flights, reallocate spend across DSPs, and report — with a human approving milestones rather than clicks. Early pilots from holding companies and ad-tech vendors are running in 2026, mostly on lower-risk performance budgets.

The tradeoffs are real. Black-box bidding hides where your dollars land. Prompts and first-party data can leak into shared model training unless contracts say otherwise. Brand safety controls in agentic workflows are still immature. Quality governance now correlates directly with results — the ANA Q4 2025 Programmatic Transparency Benchmark reports that advertiser case studies show that optimizing toward quality‑adjusted metrics, rather than CPM alone, delivered nearly 40% reductions in cost per conversion, even when nominal CPMs increased.

Your 2026 AI readiness checklist:

- Audit which platforms can train on your data and turn it off in writing

- Run Advantage+ and Performance Max against manual benchmarks for at least one quarter

- Require log-level or impression-level reporting from any DSP-side AI tool

- Keep brand campaigns, crisis response, and new-category launches human-led

- Pilot one agentic workflow on a contained performance budget, not your flagship brand

Treat AI media buying as a co-pilot in 2026. Hand it the repetitive optimization work; keep strategy, brand voice, and risk calls on your side of the table.

My rule on Performance Max and Advantage+ is simple: never give them the whole budget on day one. On a recent DTC test we ran PMax at 40% of paid search budget for six weeks against a manual shopping baseline, and only then scaled. The trap I see junior buyers fall into is feeding PMax broad asset groups with no negative keyword strategy — three weeks later half the spend is on brand terms and the dashboard looks fantastic. Strip out brand traffic before you judge incrementality, or you’re paying a tax for clicks you already had.

Principal media buying and the transparency problem

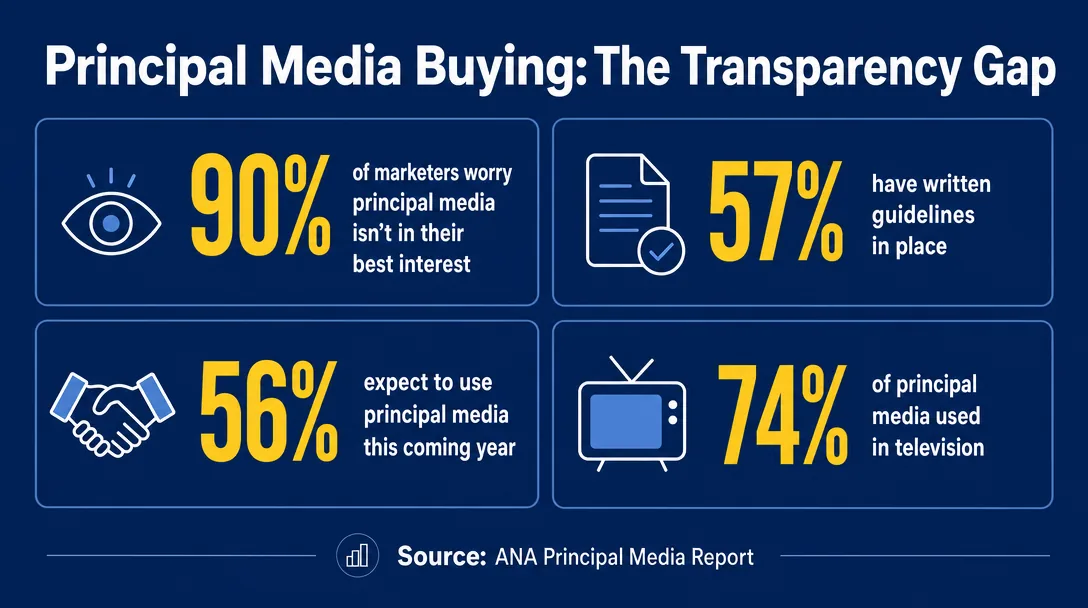

Principal media buying is when your agency stops acting as your agent and becomes a counterparty: it buys ad inventory in bulk for its own book, then resells it to you at a markup it doesn’t have to disclose. The economics flip — the agency now profits from the spread, not just your fee.

The latest ANA report on the practice makes the scale clear. Only 57 percent of marketers say their companies have guidelines governing principal media, even as 90 percent say their top concern is whether recommended principal media is truly in their best interest, up from 79 percent in the ANA’s 2024 foundational study. At the same time, 56% expect to use principal media in the coming year, compared with 41% in the earlier study, and 37% say their company’s use of principal media increased in the past year, up from 24% previously. The same report finds principal media is most commonly used in large-scale environments such as television (74%) and the digital open web (43%), where agencies can purchase inventory in bulk and resell it across multiple clients.

The risks are structural: hidden margins on resold inventory, conflicts of interest when the agency steers spend toward what it already owns, and pricing you can’t benchmark against the open market. According to Marketing Dive, more than one-third of surveyed marketers said their contracts with agencies do not address principal media or they were otherwise unsure on the matter. Made-for-advertising (MFA) sites often end up in these bundles because they’re cheap to acquire and pad performance metrics.

If principal buying is on the table, your agency contracts need teeth. Negotiate these clauses before signing:

- Disclosure requirement — written notice every time principal inventory is used in your plan

- Audit rights — your auditor can inspect invoices, markups, and inventory sources

- Opt-out language — you can decline principal buys on any campaign, no penalty

- MFA-free commitment — explicit exclusion of made-for-advertising domains

- Margin caps or pass-through pricing — defined economics, not open-ended markup

- Conflict-of-interest disclosure — agency reveals ownership stakes in any vendor it recommends

Without these, you’re not buying media — you’re buying whatever’s most profitable for the agency to sell you.

Retail Media Networks: the channel reshaping US ad budgets

Retail media networks (RMNs) are the third major wave of digital ad spend after search and social, pulling a rapidly growing share of US digital ad dollars in 2026. The pitch is simple: buy ads where shoppers are already deciding what to put in the cart, and tie those impressions to actual sales.

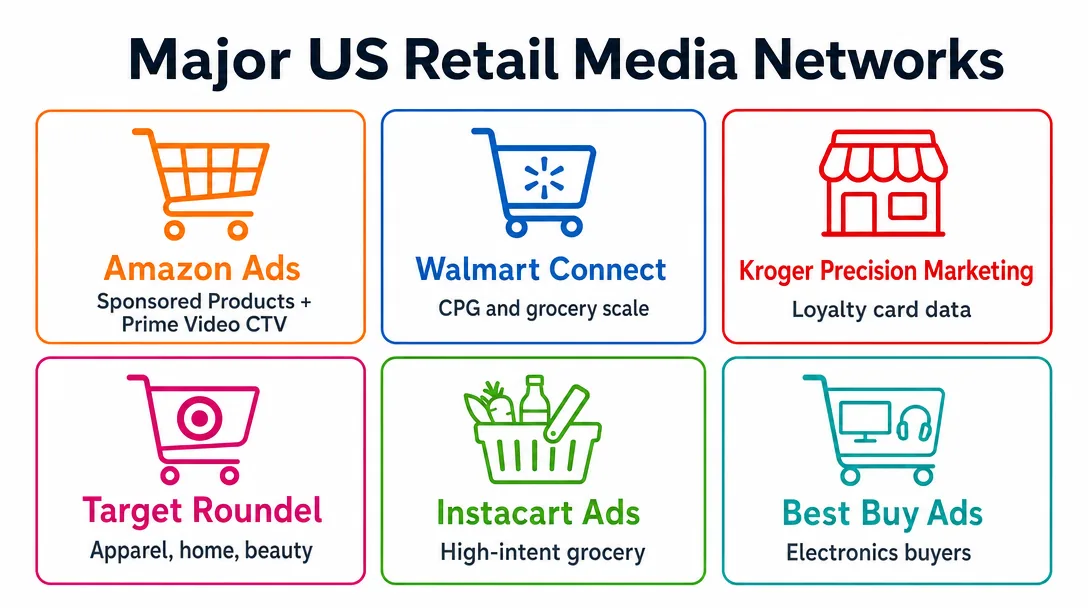

The major US players each bring a different audience and data set:

- Amazon Ads — the anchor of the category, with sponsored products, DSP access, and Prime Video CTV inventory.

- Walmart Connect — the biggest offline-to-online footprint, strong on CPG and grocery.

- Kroger Precision Marketing — loyalty-card purchase data across tens of millions of US households via the 84.51° data unit.

- Target Roundel — premium guest data, strong in apparel, home, and beauty.

- Instacart Ads — high-intent grocery shoppers across the Instacart marketplace and partner retailer banners.

- Best Buy Ads — consumer electronics and appliance buyers, narrow but deep.

What you get that the open web can’t deliver: closed-loop sales attribution and logged-in first-party data tied to real purchases, not modeled cohorts. You can buy three ways — self-serve dashboards, managed service through the retailer’s team, or programmatically through a DSP.

The catch: every RMN is a walled garden, cross-network measurement is still maturing, and standardized metrics across retailers don’t yet exist.

Privacy, signal loss, and measurement in 2026

Measurement in 2026 runs on consented first-party data, modeled attribution, and clean room collaboration — not the deterministic cookie graphs you relied on five years ago. If your stack still leans on last-click and third-party pixels, your numbers are already wrong.

The regulatory floor keeps rising. CCPA and CPRA cover California, and comparable laws are now live in Virginia, Colorado, Connecticut, Utah, Texas, Oregon, and a growing list of other states. Each adds opt-out signals, sensitive data rules, and consumer rights workflows your ad ops team has to honor.

Chrome’s third-party cookie deprecation timeline has shifted repeatedly, but the cookieless future is already here in practice: Safari and Firefox block by default, and iOS ATT gutted mobile signal years ago.

What to actually do:

- Move budget decisions to media mix modeling and geo-based incrementality tests, not last-click.

- Stand up first-party data capture across site, CRM, and loyalty, with clear consent.

- Use clean rooms — AWS Clean Rooms, Snowflake, LiveRamp — to match audiences with retailers and publishers without sharing raw PII.

- Treat platform-reported conversions as one input, not truth.

Solid attribution modeling in 2026 is triangulation, not a single number.

Agency, in-house, or hybrid? Choosing your US media buying model

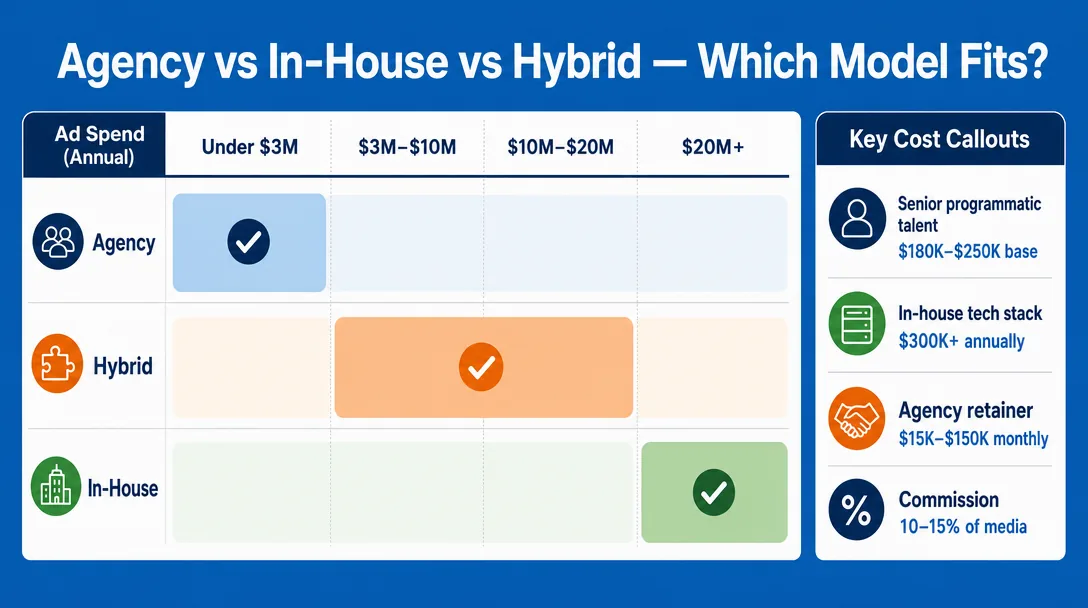

The right model depends on three variables: annual ad spend, channel mix, and how much first-party data you own. Brands under $2M in working media usually do better with an agency. Brands above $20M with strong data infrastructure often bring core channels in-house. Most fall in the middle and run hybrid.

When an agency makes sense

Media buying agencies in the US bring scale advantages you can’t replicate quickly: negotiated rates with broadcasters, direct DSP seats, and vendor relationships built over decades. You also get a tested measurement stack on day one. The trade-offs are fees and visibility. Standard pricing models include commission (10–15% of media), monthly retainer ($15K–$150K depending on scope), performance-based fees, and principal-based buying — where the agency resells inventory it bought at a markup. The last one is where transparency gets murky.

When in-house wins

In-house media buying gives you full data ownership, real-time decisioning, and no agency markup. The catch: senior programmatic talent in New York or LA runs $180K–$250K base, and your tech stack (DSP, DMP, attribution, verification) easily clears $300K annually before media. Cash flow infrastructure also matters more than most teams expect — DSPs, ad platforms, and SaaS vendors all need funded payment methods, and growing teams often turn to virtual cards and credit lines built for media buyers to keep campaigns from stalling at month-end.

The hybrid play

Most growth-stage brands keep paid search and paid social in-house — where iteration speed matters — and use boutique agencies or larger shops for CTV, linear, audio, and programmatic display. Strategy, planning, and upfront negotiations sit with the agency; daily optimization sits with your team.

Vet any US agency with these questions before you sign:

- Which DSPs do you operate, and do we get our own seats?

- Do you engage in principal-based buying? If yes, where, and how is it disclosed?

- What’s your CTV and retail media network experience by platform?

- Which attribution and incrementality vendors do you use?

- How is our first-party data stored, and who owns the audience segments at contract end?

- What rebates, AVBs, or media credits do you receive from vendors?

- Can we audit log files and bid-level data?

- Who specifically — not which team — works on our account day-to-day?

The bottom line

The US ad market in 2026 rewards buyers who can move money fast across programmatic, retail media, CTV, and search without losing sight of incrementality. The Omnicom–IPG merger reshaped agency leverage, AI agents now handle bid logic and creative variants at scale, and retail media networks keep pulling budget away from open-web display. Your edge comes from clean first-party data, honest measurement, and contracts that expose principal-buying markups before they eat your margin.

Pick one campaign running right now, pull the last 30 days of placement-level spend, and flag every line item where you can’t trace fees, data costs, or incremental lift — that short list is your media buying in the United States priority for next week.

Content verified by expert

On December 31, 2024, Dmitrii left his position as Head of Media Projects at ADSBASE Group. He currently leads CPA.LIVE and the ADDSET forum.

Holding numerous certificates, Dmitrii confirms his authority in digital marketing.

Dmitrii Medvedko Author

An expert deeply immersed in the affiliate industry. She has managed media projects such as CPA Mafia, CyberAff, ProTraffic, AffTimes, CPA Monstro, and Affiliate Valley, and gained hands-on experience in the nutra segment through the WebVork affiliate network.